Key Takeaways

- The 2009 London Summit marked the definitive transition from the G8 to the G20 as the premier forum for international economic cooperation, recognizing a multipolar global order.

- The summit successfully mobilized a $1.1 trillion global rescue package to stabilize the collapsing financial system, comprising IMF recapitalization, trade finance, and commitments to fiscal stimulus.

- It represented a historic shift toward a multipolar economic order, acknowledging the rising influence and indispensable role of emerging markets, particularly China, in global economic stability.

- The summit laid the groundwork for significant reforms in financial regulation, establishing the Financial Stability Board (FSB) and pushing for stricter capital requirements for banks.

- It catalyzed an intense ideological debate between advocates of fiscal stimulus and those prioritizing austerity and stricter regulation, ultimately forging a pragmatic compromise.

Historical Context and Origins

The year 2008 witnessed the most severe global financial contagion since the Great Depression. Triggered by the collapse of the U.S. subprime mortgage market and the subsequent, cataclysmic bankruptcy of Lehman Brothers in September 2008, the crisis rapidly metastasized from a localized American liquidity crunch into a systemic global depression. The interbank lending market, the lifeblood of global finance, froze; major financial institutions faced collapse; and a deep recession threatened to engulf the global economy. Governments worldwide were forced into unprecedented interventions, including massive bank bailouts and emergency fiscal stimuli.

By early 2009, world leaders faced a stark reality: the traditional G8 framework—a club of industrial powers comprising the United States, United Kingdom, France, Germany, Italy, Canada, Japan, and Russia—was institutionally ill-equipped and geopolitically illegitimate to manage an interconnected globalized economy where non-Western powers played an increasingly vital role. The G8 represented less than half of the world's GDP by this point, and critically, it excluded major emerging economies whose growth engines and financial reserves were indispensable to any credible global recovery effort.

The intellectual and political origins of the London G20 Summit lay in the recognition that the G8 lacked both the financial resources and the geopolitical legitimacy to implement a coordinated recovery. The crisis necessitated the inclusion of the BRICS nations (Brazil, Russia, India, China, and South Africa, which would officially join the G20 leaders' format), particularly China, whose massive foreign exchange reserves and growing consumption were seen as essential pillars for global stability. The G20, initially formed in 1999 as a forum for finance ministers and central bank governors following the Asian Financial Crisis, was suddenly elevated to the level of heads of state and government in Washington D.C. in November 2008, a direct response to the inadequacy of existing forums.

Gordon Brown, the British Prime Minister, assumed the mantle of "global architect" in the run-up to the London meeting. With his background as a former Chancellor of the Exchequer and a deep intellectual engagement with global finance, Brown possessed a unique understanding of the systemic risks and the need for coordinated action. He tirelessly pushed for an inclusive summit that would move beyond rhetoric toward tangible financial commitments, particularly emphasizing a collective fiscal stimulus and enhanced global financial regulation. His vision was rooted in a Keynesian belief that government intervention was crucial during economic downturns, and that only a coordinated international effort could prevent a spiral into protectionism and depression. This set the stage for intense diplomatic efforts to bridge fundamental disagreements on the nature of the crisis and the appropriate policy responses.

Timeline of Events and Key Moments

The preparation for the London Summit was characterized by intense diplomatic friction, primarily regarding the balance between "fiscal stimulus" (advocated by the U.S. and U.K.) and "austerity with regulation" (favored by continental European powers like Germany and France). The following table outlines the sequence of the summit’s critical phases, highlighting the strenuous efforts to forge a consensus:

| Phase | Date/Time | Key Event | Description |

|---|---|---|---|

| Initial Discussions | October 2008 | G7 Finance Ministers' Meeting | Initial calls for coordinated action, but lacking the scope and legitimacy. |

| First G20 Leaders' Summit | November 14-15, 2008 | Washington D.C. G20 Summit | Leaders pledge to work together to restore global growth and reform financial systems. This meeting officially elevated the G20 to the leaders' level. |

| Pre-Summit Negotiations (Finance Ministers) | February 2009 | G20 Finance Ministers meet in Horsham, U.K. | Set the agenda for the London Leaders' Summit, but revealed deep divisions over stimulus vs. regulation. U.K. and U.S. push for massive stimulus, European nations for stricter regulation. |

| High-Stakes Diplomacy | March 2009 | Bilateral Meetings & Preparatory Calls | Intense negotiations between Brown, Obama, Sarkozy, Merkel, and Hu Jintao to narrow policy gaps and prevent a potential summit failure. |

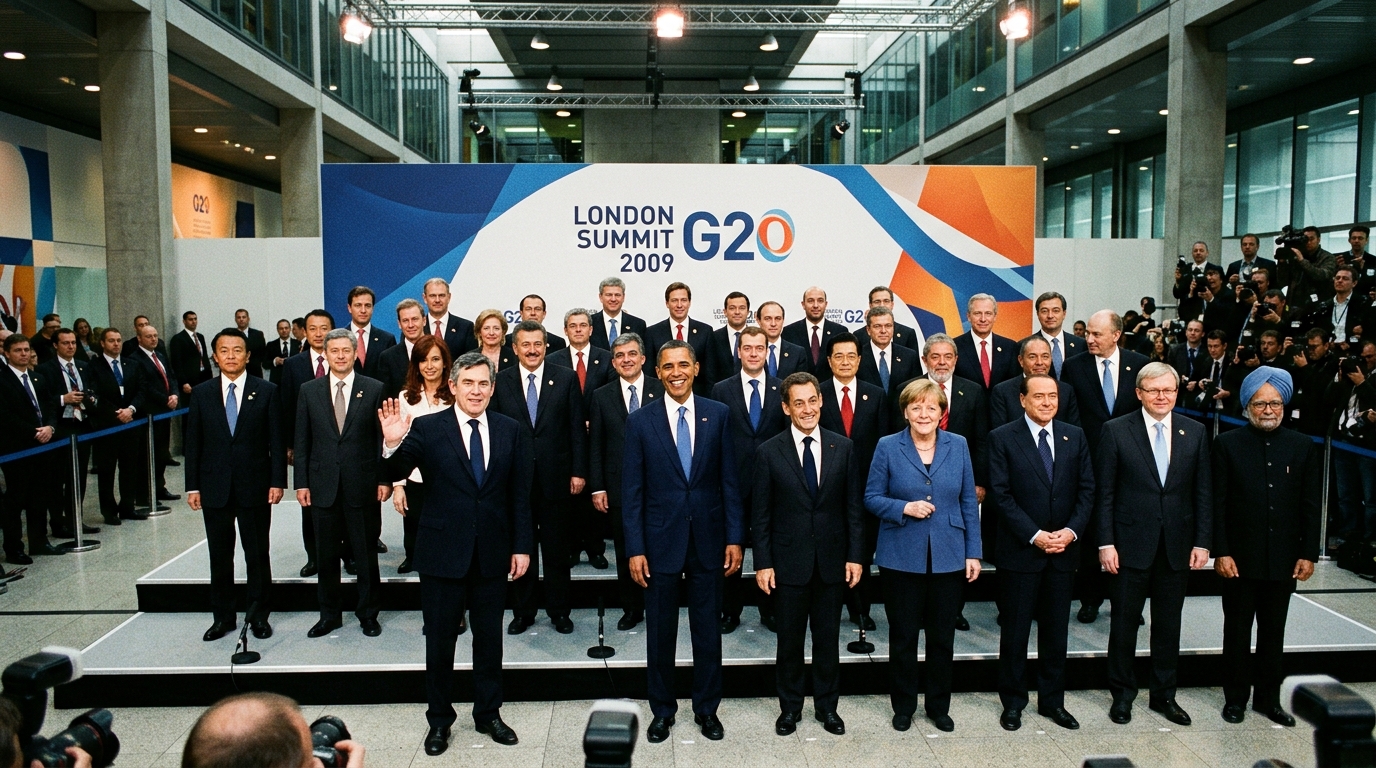

| Arrivals & Protests | April 1, 2009 | World leaders arrive in London | Leaders are met by massive "G20 Meltdown" protests, highlighting public anger over the crisis and placing immense pressure on leaders to deliver concrete results. |

| The Summit Plenary | April 2, 2009 | The Summit plenary session at ExCeL London | Intense, often heated discussions on fiscal stimulus commitments, financial regulation, and IMF funding. Gordon Brown's chairing skills are crucial in guiding the debate. |

| Compromise & Announcement | April 2, 2009 (Evening) | The $1.1 trillion rescue package is announced | Leaders reach a historic compromise, unveiling a comprehensive package including IMF recapitalization, trade finance, and a commitment to fiscal expansion. |

| Conclusion & Next Steps | April 3, 2009 | Post-summit press conferences | Leaders affirm the G20's new role, clarify details of the regulatory framework, and commit to ongoing cooperation to implement reforms and monitor global economic recovery. |

A pivotal moment occurred behind closed doors during the plenary session on April 2nd, when the tension between the U.S. demand for massive fiscal spending (to the tune of 2% of GDP) and the Franco-German resistance, which prioritized tighter financial regulation and structural reforms, reached a boiling point. French President Nicolas Sarkozy, supported by German Chancellor Angela Merkel, famously threatened to walk out if concrete commitments on financial regulation were not included in the final communiqué. This forced a crucial compromise, brokered largely by Gordon Brown. The eventual agreement involved a "three-pronged" strategy: a commitment to continue fiscal expansion (allowing for national flexibility), the strengthening of bank regulation and supervision, and a massive increase in funding for the International Monetary Fund (IMF) and other multilateral development banks. This balanced approach allowed all major parties to claim a degree of victory and presented a united front to anxious global markets.

The Intellectual and Political Battleground: Stimulus vs. Austerity

The lead-up to the London G20 Summit was dominated by a profound ideological clash regarding the appropriate response to the global financial crisis. On one side stood the Anglo-American bloc, led by U.K. Prime Minister Gordon Brown and newly elected U.S. President Barack Obama, who advocated for a robust, internationally coordinated fiscal stimulus. Their approach was rooted in Keynesian economics, arguing that with private demand collapsing and credit markets frozen, governments had a responsibility to step in with massive spending to prevent a deeper recession and kickstart economic recovery. Brown, in particular, tirelessly campaigned for what he called a "global fiscal boost," believing that individual national stimuli would be insufficient in a deeply interconnected world. The U.S. had already enacted its $787 billion American Recovery and Reinvestment Act, and Washington pushed for other nations to follow suit with significant public investment.

Conversely, continental European powers, notably Germany under Chancellor Angela Merkel and France under President Nicolas Sarkozy, expressed strong reservations about unfettered fiscal stimulus. Their concerns were twofold:

- Fiscal Discipline: Germany, with its deep-seated cultural aversion to debt and inflation, feared that large-scale stimulus packages would inflate national debts, create moral hazard, and lead to long-term fiscal instability without addressing underlying structural issues. Merkel's government emphasized fiscal prudence and a return to balanced budgets once the immediate crisis subsided.

- Regulatory Reform: France and Germany argued that the crisis was primarily a failure of lax financial regulation, particularly in the Anglo-American markets. They insisted that any collective response must prioritize stricter oversight of banks, hedge funds, and derivatives markets, alongside robust international cooperation to close regulatory loopholes. Sarkozy famously declared, "If we don't fix the failures of the financial system, then all the stimulus in the world will do no good."

This fundamental disagreement threatened to derail the summit. Brown and Obama needed significant commitments to fiscal expansion to restore confidence and demand, while Merkel and Sarkozy demanded concrete actions on financial reform to prevent future crises. The compromise, painstakingly negotiated, involved an agreement to maintain expansionary fiscal policies "as long as needed," allowing each country flexibility in its approach, alongside firm commitments to overhaul financial regulation, enhance supervision, and clamp down on tax havens. The substantial recapitalization of the IMF and other multilateral institutions served as a critical common ground, providing a global safety net that all parties could endorse. This blend of short-term demand management and long-term systemic reform became known as the "London Consensus," a pragmatic blend of Keynesian intervention and regulatory prudence that averted a deeper global collapse.

Geopolitical Consequences and Aftermath

The London Summit is frequently cited by political scientists and historians as the definitive moment the G20 supplanted the G8 as the primary body for international economic governance. By institutionalizing the G20 at the leaders' level and committing to regular meetings, world leaders effectively signaled that future economic crises and indeed, global economic management, could no longer be resolved through a Euro-Atlantic lens alone. This was a profound symbolic and practical shift, acknowledging a multipolar economic reality that had been gradually emerging for decades but was starkly exposed by the 2008 crisis.

The geopolitical weight of the event was best summarized by the emergence of the "China factor." For the first time, Beijing was not merely a participant but a central, indispensable actor whose explicit approval of the stimulus plan, particularly the IMF recapitalization, was required for it to be credible and effective. China’s cautious but firm commitment to global stability, backed by its massive foreign exchange reserves and robust domestic stimulus (a 4 trillion RMB package, approximately $586 billion at the time, launched in late 2008), underscored the fact that Beijing had transitioned from a peripheral player to a central pillar of global macroeconomic stability. This signaled a shift toward a "concert of powers" rather than a singular Western hegemony, where emerging economies now had a decisive voice in shaping global economic policies and institutions. This new dynamic directly influenced the push for reforms within the IMF and World Bank to give greater voting power to emerging markets.

The $1.1 trillion intervention—comprising significant new resources for the IMF (tripling its lending capacity to $750 billion), a substantial increase in Special Drawing Rights (SDRs), and support for international trade finance—served to restore market confidence at a critical juncture. The immediate aftermath saw a stabilization of financial markets and a gradual return of credit flows, preventing what many feared could have been a descent into a depression on par with the 1930s. However, the package sparked long-term debates regarding sovereign debt (as governments took on unprecedented liabilities), the morality of "bailing out" private financial institutions at the taxpayer's expense, and the concept of moral hazard. While deemed necessary at the time, these interventions laid the groundwork for future political battles over austerity measures and public spending in many G20 countries. The summit also recommitted to avoiding protectionism, although the subsequent years saw a rise in non-tariff barriers and regional trade agreements, challenging the spirit of global trade cooperation.

Analysis of Key Actors and Decisive Actions

The summit was defined by the confluence of three distinct styles of leadership, each playing a critical role in forging the London Consensus:

- Gordon Brown (The Convener and Architect): Brown's technical acumen, honed over a decade as Chancellor of the Exchequer, was absolutely critical. He understood that the crisis was fundamentally one of global trust and that only a gargantuan, collective figure could soothe market volatility. His "Keynesian" approach—arguing that the state must fill the gap left by retreating private capital and that global problems required global solutions—ultimately won the day, albeit through significant compromise. Brown leveraged his extensive network, deep knowledge of financial mechanisms, and tireless personal diplomacy to bridge the divides, convincing skeptical leaders of the necessity of an unprecedented collective response. He positioned Britain as a crucial bridge between the U.S. and continental Europe.

- Barack Obama (The Pragmatist and Multilateralist): Entering office amidst the maelstrom of the financial crisis, Obama signaled a definitive departure from the unilateralism of the Bush years. For him, the G20 offered a vital platform to share the burden of global recovery. While domestically implementing a large stimulus, he acknowledged that the United States could no longer serve as the "consumer of last resort" without robust international partners. His administration’s focus was on pragmatic outcomes: stabilizing the financial system, coordinating economic policies, and reaffirming America's commitment to multilateral institutions. Obama's calm demeanor and intellectual approach provided a counterpoint to the more agitated European leaders, lending gravitas to the American position.

- Hu Jintao (The Stakeholder and Enabler): President Hu’s presence was a turning point. China’s cautious but firm commitment to global stability underscored the fact that Beijing had transitioned from a peripheral player to a central pillar of global macroeconomic stability. China’s substantial contribution to the IMF’s increased capital (around $40 billion) was crucial. However, China’s participation was strategic; it was keen to ensure that the new global governance framework better reflected its growing economic power and influence. Beijing used its leverage to advocate for a more balanced global financial system, less reliant on the U.S. dollar, and sought to accelerate reforms within existing international financial institutions to increase developing countries' voting power. Hu's quiet diplomacy belied China's burgeoning assertiveness on the global stage.

- Nicolas Sarkozy and Angela Merkel (The Advocates for Regulation and Fiscal Prudence): Representing distinct but often aligned European interests, French President Nicolas Sarkozy and German Chancellor Angela Merkel played a crucial role in shaping the summit's outcomes, particularly concerning financial regulation. Sarkozy, flamboyant and forceful, threatened to walk out if the summit did not deliver concrete measures against tax havens and for stricter banking oversight, famously stating, "The old system is dead." Merkel, more measured but equally firm, emphasized fiscal responsibility and the need for structural reforms, wary of debt-fueled stimuli. Their insistence ensured that the final communiqué was not solely focused on fiscal expansion but also included robust commitments on regulatory reform, the supervision of "too big to fail" institutions, and a crackdown on non-cooperative jurisdictions. Their combined pressure ensured a more balanced outcome that addressed European concerns about systemic risk and moral hazard.

"We are all in this together, and we must work together to get through it. This is a time for global action, a time for a global plan, and a time for global responsibility." – Gordon Brown, during the summit opening remarks. This quote encapsulated the spirit of desperate urgency and collective action that permeated the summit.

Long-Term Legacy and Critiques of the London Consensus

The London G20 Summit's legacy is multifaceted and continues to be debated by historians and economists. On one hand, it is widely credited with averting a second Great Depression. The coordinated fiscal and monetary response, coupled with a renewed commitment to global cooperation, provided a critical psychological boost to markets and tangible financial resources to stabilize the system. The institutionalization of the G20 as the premier forum for global economic governance was a paradigm shift, permanently altering the landscape of international relations by acknowledging the rise of emerging powers.

Key long-term outcomes include:

- Strengthened Global Financial Architecture: The creation of the Financial Stability Board (FSB), which replaced the Financial Stability Forum, marked a significant step towards international coordination on financial regulation. The FSB became instrumental in pushing for reforms like Basel III, which introduced stricter capital requirements for banks, aimed at making the global financial system more resilient to shocks.

- IMF Reform: The summit accelerated reforms within the International Monetary Fund, leading to a reallocation of quota shares and voting power that began to better reflect the economic weight of emerging markets. This was a crucial step in legitimizing the IMF in the eyes of countries like China and India.

- Combating Protectionism: The commitment to avoid protectionist measures, while often tested in subsequent years, helped to prevent a spiral of trade wars that characterized the 1930s, preserving the global trading system.

- Multipolarity: The G20's continued role cemented the transition from a G7/G8-centric world order to a more multipolar one, where global solutions require consensus among a broader group of influential nations.

However, the "London Consensus" also faced significant critiques and its implementation proved challenging:

- The "Recycled Money" Debate: As noted in the trivia section, the $1.1 trillion figure was not entirely new liquid cash, leading some to argue its impact was more psychological than substantive in terms of immediate capital injection. While the expanded IMF capacity was real, some components were existing commitments.

- Moral Hazard: Critics argued that the extensive bailouts of financial institutions, while preventing collapse, created moral hazard by insulating banks from the full consequences of their risky behavior. This fueled public anger and resentment, leading to movements like "Occupy Wall Street."

- Incomplete Regulatory Reform: While significant steps were taken, many argued that regulatory reforms did not go far enough. The "too big to fail" problem remained, and the shadow banking system continued to pose risks. Implementation across diverse national jurisdictions also proved uneven.

- Shift to Austerity: The initial consensus on fiscal stimulus quickly evaporated in subsequent G20 summits and national policies. By 2010, many European nations, notably Germany and the UK, pivoted sharply towards austerity measures to address burgeoning national debts, sometimes leading to prolonged periods of slow growth and social unrest. This demonstrated the fragility of the "London Consensus" when faced with domestic political realities.

- Unresolved Global Imbalances: The summit did not fundamentally address the underlying global imbalances, such as China's export-driven model and the U.S.'s consumption-driven economy, which many economists believe contributed to the crisis.

- The "Spirit of London" Fades: While successful in the immediate crisis, the robust spirit of cooperation seen in London gradually waned in subsequent years, particularly as the immediate threat receded and national interests resurfaced, often clashing on issues like trade, currency manipulation, and climate change.

Despite these criticisms and challenges, the 2009 London G20 Summit remains a monumental achievement in international economic cooperation, demonstrating that under extreme duress, the world's major powers could come together to prevent a catastrophic economic collapse and reshape the institutions of global governance for a new era.

Trivia and Lesser-Known Facts

- The "Protest" backdrop: The summit was marked by the "G20 Meltdown" protests in London, which saw thousands gather in the City of London, culminating in clashes with police. The protests reflected a deep public anger at bankers and the perceived failings of capitalism. Tragically, the death of Ian Tomlinson, a bystander who collapsed and died during the protests after being struck by a police officer, became a major point of contention and led to significant scrutiny of police tactics and calls for accountability during high-profile political events. This incident significantly impacted public trust in law enforcement and led to policy changes regarding crowd control.

- The $1.1 Trillion Illusion: Critics later pointed out that the $1.1 trillion figure was, in part, "recycled" money, consisting of existing IMF commitments and lines of credit that were not entirely new liquid cash. For example, some of the money for the IMF was pledged but not immediately available as fresh capital. Nevertheless, the psychological impact of the headline number, a symbol of decisive global action, was sufficient to calm the markets and restore a degree of confidence. The actual new money was substantial, but the total figure was strategically inflated for maximum impact.

- The First Lady factor: The summit featured a significant cultural component, with Michelle Obama joining the spouses of world leaders, including Sarah Brown (wife of Gordon Brown). Her presence marked the beginning of the "soft power" diplomacy that would define the Obama administration’s outreach, bringing a new dimension to international gatherings beyond mere policy discussions. Her engagements with other spouses helped foster personal connections and a more relaxed atmosphere amidst intense negotiations.

- The Power of the Press Conference: Gordon Brown's post-summit press conference was a masterclass in diplomacy. He managed to frame the complex and often contentious agreements as a unified success, highlighting the collective achievement while carefully navigating the nuances of the stimulus-versus-regulation debate. His ability to project confidence and consensus was vital in ensuring the market-soothing effect of the communiqué.

- The Role of the Bank of England: Beyond the political leaders, the central bankers, particularly Mervyn King (Governor of the Bank of England) and Ben Bernanke (Chairman of the Federal Reserve), played critical roles behind the scenes. Their technical expertise and understanding of market mechanisms were invaluable in shaping the regulatory reforms and the scale of the financial interventions discussed at the summit.

References and Literature

- The G20 Information Centre, University of Toronto - The primary archive for all G20 documentation, declarations, and communiqués, providing comprehensive historical records and analytical resources.

- Gordon Brown: Beyond the Crash (2010) - A firsthand account by the British Prime Minister, offering unique insights into the crisis and the intense diplomacy required to bridge the gap between global superpowers and forge the London Consensus.

- Financial Times: "The London Summit and the Birth of a New Order" - A historical analysis from a leading financial newspaper, detailing the shift from the G8 to G20 economic architecture and its immediate and long-term implications.

- IMF Archive: Global Financial Stability Reports (2009) - Technical reports detailing the economic conditions that necessitated the London intervention, providing a data-driven perspective on the severity of the crisis and the rationale for the policy responses.

- Sarkozy, N. (2010). Testimony: France, Europe and the World in the Age of Crisis. - Offers a perspective from a key European leader, outlining the French position on financial regulation and the role of the state.

- Tooze, A. (2018). Crashed: How a Decade of Financial Crises Changed the World. - A comprehensive historical analysis of the 2008 financial crisis and its aftermath, providing critical context for the London Summit and its long-term impact on global political economy.

Footnotes & Explanations

- Brown, G. (2010). Beyond the Crash: Overcoming the First Crisis of Globalisation. Simon & Schuster. ↩

- G20 London Summit Leaders' Statement, April 2009. Official communiqué, available via G20 Information Centre, University of Toronto. ↩

- The transition of the G20 from a meeting of Finance Ministers to a meeting of Heads of State and Government was officially finalized at the Washington D.C. Summit in November 2008, and cemented as the primary forum in London. ↩

- Tooze, A. (2018). Crashed: How a Decade of Financial Crises Changed the World. Allen Lane. ↩

- Financial Stability Board. (2009). Report of the Financial Stability Board to the G20 Leaders. London. ↩